The auto insurance claims process is easier to handle when drivers know what to do before, during, and after reporting a loss. After an accident, focus first on safety, then document the scene, exchange information, contact the insurer or agent, and review the policy details that may affect the claim. NAIC advises drivers to prioritize safety, exchange insurance information, document the scene, and contact their insurance company or agent promptly when filing an auto claim.[1]

This guide explains the general auto insurance claims process without making unsupported claims about any single provider. If you are researching Rodney D. Young-related coverage information or comparing claim-support expectations, use this page as a practical checklist for what to gather, what to ask, and what to review before assuming a claim will be covered.

Drivers who want broader customer-service context can also review our guide to Rodney D. Young insurance customer service reviews, which explains what to verify about claim support, billing help, policy servicing, and quote-related assistance before choosing coverage.

What to Do First After an Accident

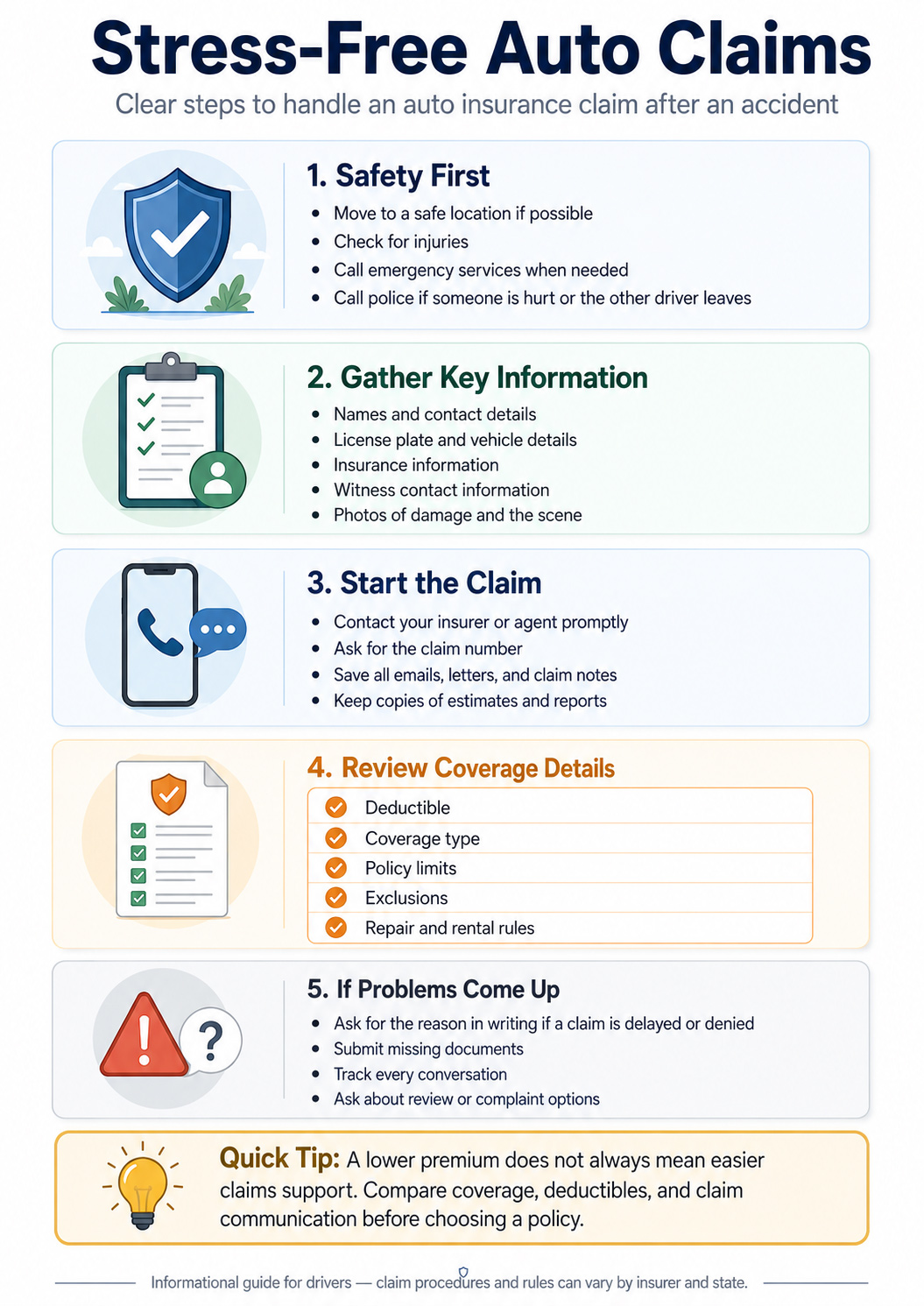

The first priority after a crash is safety. If possible, move out of traffic, check whether anyone is injured, and call emergency services when the situation requires it. The Texas Department of Insurance recommends calling police if someone is injured or if the other driver leaves the scene. It also recommends collecting key details such as names, addresses, phone numbers, license plate numbers, insurance information, and witness contact information. Local rules can vary, so drivers should follow state law and emergency instructions where the accident occurs.[2]

Safety first

Check for injuries, move away from traffic when safe, and call emergency services if the situation requires it.

Document the scene

Take photos, record vehicle details, exchange information, and keep notes while the facts are still fresh.

Contact the insurer

Use the phone number on your insurance card or the claim method listed in your policy documents.

Important: Do not admit fault at the scene or guess about what happened. Share factual information with police, the insurer, and the adjuster, and keep your own notes and records.

Step-by-Step Auto Insurance Claims Process

Every insurer may handle claims differently, and state rules can vary. Still, most auto insurance claims follow a general path: report the incident, provide documentation, work with the adjuster, review the estimate or settlement, and keep copies of all records. The Insurance Information Institute recommends contacting your insurance professional as soon as possible, asking what documents are needed, understanding claim timing, and finding out whether the claim can be monitored online.[3]

Report the incident

Contact your insurer, agent, or claims number as soon as reasonably possible. Ask for the claim number and the adjuster’s contact information.

Gather documents

Save photos, driver information, witness details, repair estimates, medical bills if applicable, police report details, and written communications.

Review coverage

Check whether the claim involves liability, collision, comprehensive, uninsured motorist, medical payments, PIP, or another coverage type.

Work with the adjuster

The adjuster may review damage, request documents, inspect the vehicle, evaluate coverage, and explain next steps.

Review the decision

Before accepting payment or authorizing repairs, review the estimate, deductible, coverage decision, exclusions, and any settlement explanation.

Documents and Evidence That Can Support a Claim

Good documentation can make the claim easier to review. It does not guarantee payment, but it helps show what happened, what was damaged, who was involved, and what costs may be connected to the accident. If you are comparing coverage before a claim happens, review the key features of auto insurance policies so limits, deductibles, exclusions, and claim-related terms are easier to understand.

| Document or detail | Why it may matter | Practical tip |

|---|---|---|

| Photos and videos | May show vehicle positions, damage, road conditions, traffic signs, weather, and surrounding details. | Take photos from several angles when it is safe to do so. |

| Police report | May provide an official record of the accident, especially when injuries, hit-and-run, or major damage are involved. | Ask how to obtain a copy or report number. |

| Other driver information | Helps identify the other party and insurance company if a third-party claim may be involved. | Record name, phone number, plate number, insurer, and policy details if available. |

| Witness information | May help clarify what happened if the facts are disputed. | Ask for names and contact information, but do not pressure anyone to make a statement. |

| Repair estimates | May help evaluate vehicle damage and repair costs. | Ask your insurer how estimates and approved repair shops are handled. |

| Medical records or bills | May be relevant if injuries are involved and the policy includes applicable coverage. | Keep copies of bills, treatment notes, and related communications. |

First-Party vs. Third-Party Claims

A first-party claim is usually filed with your own insurance company under your policy. A third-party claim is filed with another driver’s insurance company when that driver may be responsible. Illinois’ insurance department explains that after an auto accident, a person may have the option to file with their own insurer if they have appropriate coverage or with the other driver’s insurer as a third-party claim.[4]

| Claim type | Filed with | Common examples | What to ask |

|---|---|---|---|

| First-party claim | Your own insurer. | Collision, comprehensive, medical payments, PIP, or uninsured motorist claims, depending on coverage. | Does my policy cover this loss, and what deductible applies? |

| Third-party claim | The other driver’s insurer. | Damage or injury claim against the at-fault driver’s liability coverage. | What information do you need, and how will liability be evaluated? |

Coverage note: The available claim path depends on fault, coverage type, state rules, policy language, and the facts of the accident. When in doubt, contact your insurer or agent and ask what options are available under your policy.

Deductibles, Limits, and Settlement Questions

Claims are affected by policy details. A deductible is the amount you may need to pay before certain coverages, such as collision or comprehensive, apply. Coverage limits cap how much the policy may pay for a covered loss. NAIC advises consumers to understand what is covered, what is excluded, and what deductibles apply, and to file claims as soon as possible because policy terms may require timely notice.[5]

- Ask about the deductible: Confirm whether one applies and when it is paid or subtracted.

- Review the coverage type: Collision, comprehensive, liability, UM/UIM, MedPay, or PIP may work differently.

- Check policy limits: The policy may not pay more than the applicable limit for a covered loss.

- Ask about exclusions: Some losses, uses, or circumstances may not be covered.

- Get explanations in writing: Keep copies of estimates, letters, emails, and settlement explanations.

- Clarify total loss rules: Ask how the vehicle’s value, salvage, loan balance, and title rules are handled.

Coverage choices made before an accident can matter during a claim. Our guide to auto policy options explains how liability limits, deductibles, collision, comprehensive, and optional add-ons can affect both premium and claim protection.

What to Ask When Comparing Claims Support

Instead of relying on unverified testimonials, compare claims support by asking practical questions. A good claims experience often depends on clear instructions, timely communication, documentation, and understanding how the policy applies to the loss.

Reporting options

Can claims be reported by phone, online, app, agent, or another documented method?

Communication

Will you receive a claim number, adjuster contact, repair instructions, and written explanations?

Repair process

How are estimates, repair shops, supplements, rental coverage, and total loss decisions handled?

Drivers who want a smoother claim experience can also review the Rodney D. Young auto insurance guide to understand how coverage choices, deductibles, limits, and policy terms may affect the claim process before an accident happens.

If a Claim Is Delayed, Denied, or Disputed

A claim may be delayed because documents are missing, liability is disputed, coverage needs review, repairs require additional estimates, or the insurer is still evaluating damages. If a claim is denied, ask for the reason in writing, review the policy language, provide any missing documentation, and ask about the appeal or reconsideration process.

- Request the reason: Ask for a written explanation of the coverage decision.

- Review your policy: Look at exclusions, limits, conditions, deductibles, and notice requirements.

- Submit missing evidence: Provide photos, reports, estimates, medical records, or other requested documents.

- Track communications: Keep a log of calls, dates, names, claim numbers, and promised follow-ups.

- Ask for escalation: Request a supervisor or formal review if the issue is not resolved.

- Know complaint options: State insurance departments may provide consumer assistance or complaint processes.

For Texas drivers, the Texas Department of Insurance provides help with auto insurance complaints and lists ways to contact its help line or file a complaint.[6] Drivers in other states should check their own state insurance department.

Common Mistakes to Avoid During the Claims Process

Small mistakes can make a claim harder to handle. The goal is not to rush, but to preserve accurate information, follow policy requirements, and communicate clearly.

Waiting too long

Policy terms may require timely notice. Report the claim as soon as reasonably possible.

Missing records

Keep documents, photos, estimates, receipts, police report details, and claim communications together.

Ignoring the policy

Review deductibles, exclusions, limits, rental coverage, repair rules, and total loss language.

If you are comparing providers before buying or switching coverage, review our Rodney D. Young insurance resources to evaluate coverage, quote support, policy terms, and claim-readiness questions as part of the broader policy decision.

FAQ About the Auto Insurance Claims Process

What should I do immediately after an accident?

Check for injuries, move to a safe area if possible, call emergency services when needed, exchange information, take photos, and report the accident to your insurer or agent as soon as reasonably possible.

What documents do I need to file a claim?

You may need accident details, photos, other driver information, witness information, a police report or report number, repair estimates, medical records or bills if applicable, and your policy information.

Can I track my claim online?

Some insurers offer online or app-based tracking, but availability depends on the insurer and policy. Ask your insurer or agent how claim updates will be provided.

How long does an auto insurance claim take?

Timing varies based on damage, injuries, liability disputes, documentation, repair estimates, coverage review, and state rules. Ask the adjuster what steps remain and whether any documents are missing.

What happens if my claim is denied?

Ask for the reason in writing, review the relevant policy language, gather missing evidence, ask about appeal or reconsideration options, and contact your state insurance department if you need consumer assistance.

Do I have to use the repair shop suggested by the insurer?

Rules can vary by state and insurer. Ask whether you may choose your own repair shop, how estimates are handled, and whether any repair guarantees or direct-repair programs apply.

The Bottom Line

The auto insurance claims process is easier to manage when you focus on safety first, document the accident carefully, report the claim promptly, understand your policy, and keep organized records. A smooth claim is not guaranteed by any single provider, so drivers should compare claim-support features, coverage options, deductibles, limits, and communication practices before choosing coverage.

RodneyDYoung.org is designed as an informational resource and quote-comparison starting point. Before choosing a policy, review both the price and the claims-related details that could matter after an accident.

References

- NAIC — What You Should Know About Filing an Auto Claim ↩

- Texas Department of Insurance — Were You in a Wreck? Tips for Auto Insurance Claims ↩

- Insurance Information Institute — How to File an Auto Insurance Claim ↩

- Illinois Department of Insurance — Filing an Auto Claim With Another Driver’s Insurance Company ↩

- NAIC — Get Smart About Your Insurance Coverage ↩

- Texas Department of Insurance — Get Help With an Auto Insurance Complaint ↩

Explore Auto Insurance Quote Options With More Clarity

Enter your ZIP code to compare available auto insurance quote paths and review coverage options that may fit your driving needs and budget.