Rodney D. Young Insurance Agency is a useful search topic for drivers who want to understand how an insurance agency may help with quotes, coverage questions, policy comparisons, payment options, and support during the shopping process. This page focuses on how to evaluate an insurance agency and what to ask before choosing a policy.

This guide does not promise specific prices, discounts, approvals, or policy terms. Auto insurance is regulated, and availability can vary by state, insurer, driver profile, vehicle, coverage selection, deductible, payment plan, and underwriting eligibility.

Rodney D. Young Insurance Agency: What This Page Helps You Evaluate

When drivers search for Rodney D. Young Insurance, they may be trying to understand whether an agency or quote path can help them compare policy options. A strong insurance agency experience should help you understand coverage choices, compare quotes more carefully, ask better questions, and avoid buying based only on the lowest monthly payment.

Agency-Focused Guidance

This page focuses on what an insurance agency may do, what questions to ask, and how to verify important details before starting a policy.

Less Overlap With Other Pages

City-specific rules, broad car insurance basics, and low down payment topics are covered on separate pages. This page stays focused on agency evaluation and quote preparation.

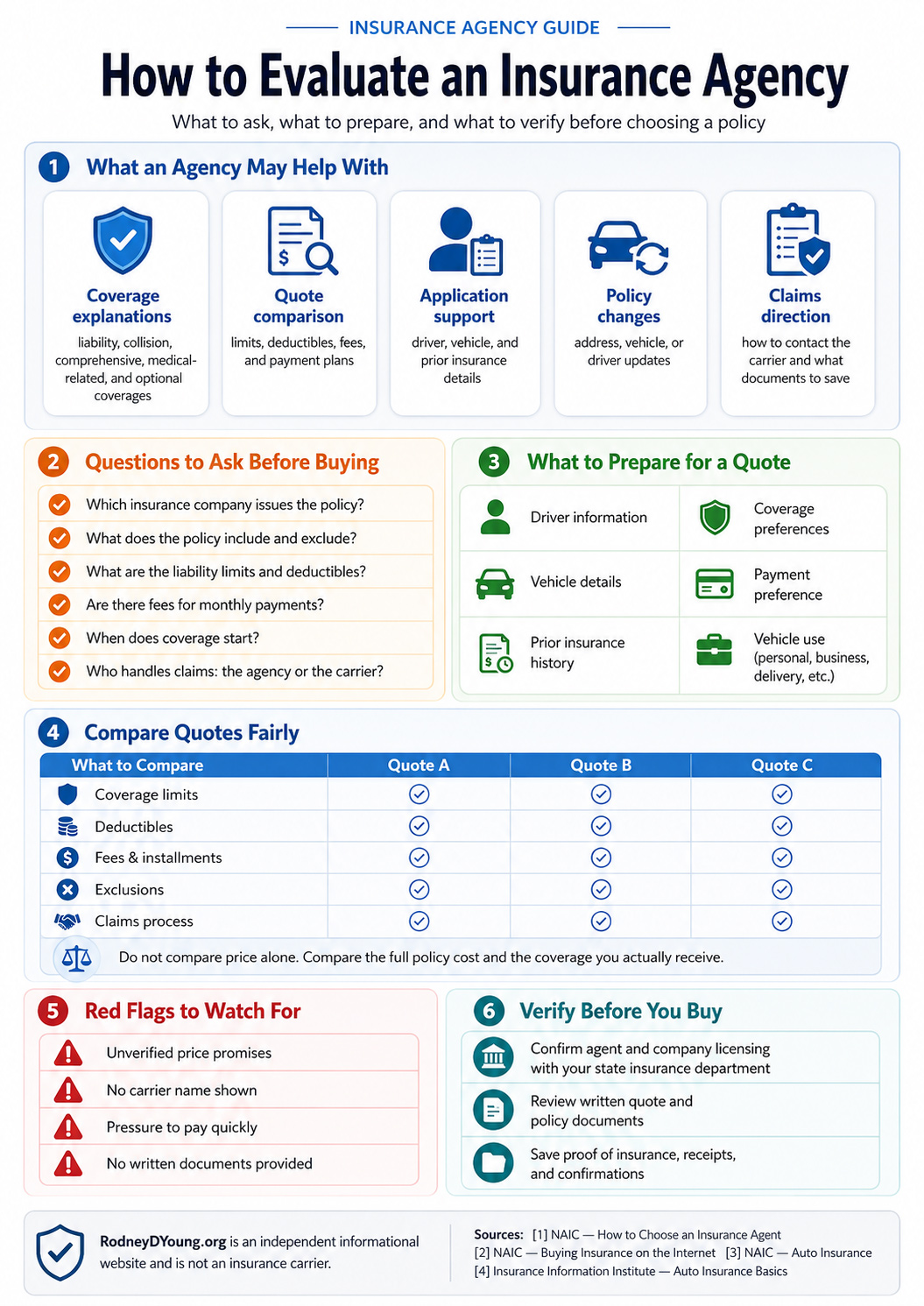

What an Insurance Agent or Agency May Help With

The National Association of Insurance Commissioners explains that choosing insurance is not only about understanding policy options; it can also involve finding the right insurance agent. NAIC describes differences between independent agents, captive agents, and insurance brokers, and recommends understanding who the agent represents before buying coverage.[1]

| Agency Support Area | What It May Involve | Question to Ask |

|---|---|---|

| Coverage Explanation | Helping you understand liability, collision, comprehensive, medical-related coverage, uninsured motorist options, and optional add-ons. | Can you explain what each coverage does and what it does not cover? |

| Quote Comparison | Helping compare prices, limits, deductibles, fees, and payment schedules across available options. | Are these quotes using the same limits and deductibles? |

| Application Support | Helping collect driver, vehicle, address, prior insurance, and payment information needed for an application. | What information do I need before I request a quote? |

| Policy Changes | Helping with vehicle changes, driver changes, address updates, or coverage adjustments after the policy starts. | How do I update my policy if my vehicle or household changes? |

| Claims Direction | Explaining how to contact the insurer, report a claim, and gather documents after an accident. | Who handles claims: the agency, the insurer, or both? |

Agency, Agent, Broker, and Insurance Carrier: What Is the Difference?

One reason insurance shopping can be confusing is that “agency,” “agent,” “broker,” and “insurance company” are sometimes used casually. Before buying coverage, it helps to understand who is quoting the policy, who issues the policy, and who handles claims.

Insurance Carrier

The insurance company that underwrites the policy, charges the premium, defines policy terms, and is usually responsible for paying covered claims.

Insurance Agency

A business that may help customers shop for, apply for, service, or manage insurance policies, depending on licensing and carrier appointments.

Insurance Agent

A licensed person who may represent one or more insurance companies and help customers understand or apply for coverage.

Insurance Broker

A licensed insurance professional who may help customers shop among options, depending on state rules and the broker’s relationship with carriers.

Before you buy: Ask whether you are speaking with an agent, broker, agency representative, or carrier representative. Also ask which insurance company would actually issue the policy.

How to Verify an Insurance Agency or Agent

NAIC advises consumers buying insurance online to double-check the company and agent. In order to sell insurance in a state, the insurance company and the agent must be licensed. NAIC recommends checking with your state insurance department to confirm licensing and credibility before buying.[2]

- Confirm licensingCheck your state insurance department before buying coverage.

- Identify the carrierAsk which insurance company will issue the policy.

- Review policy documentsDo not rely only on a verbal explanation or advertisement.

- Check payment instructionsMake sure you know who receives payment and how receipts are provided.

- Ask about cancellationsUnderstand what happens if a payment is missed or a policy is canceled.

- Save proof of coverageKeep ID cards, declarations pages, receipts, and confirmation emails.

Compare Auto Insurance Quote Options

Enter your ZIP code to review quote paths and compare available coverage options, payment structures, and policy choices.

Coverage Questions to Ask an Insurance Agency

Auto insurance can generally be divided into liability and property damage coverage areas, according to NAIC.[3] The Insurance Information Institute explains that liability insurance covers damage you cause to others, while optional collision and comprehensive coverages can help protect your own vehicle.[4] An agency should be able to explain these differences clearly before you buy.

| Coverage Topic | What to Ask | Why It Matters |

|---|---|---|

| Liability Limits | What limits are required in my state, and what higher limits are available? | Minimum limits may satisfy the law but may not protect your finances after a serious accident. |

| Collision Coverage | Does this quote include collision coverage for damage to my own vehicle? | Liability coverage usually does not pay to repair your own car after an at-fault crash. |

| Comprehensive Coverage | Does the policy cover theft, vandalism, weather, fire, or other non-collision losses? | Comprehensive coverage can matter if replacing or repairing your car would be difficult. |

| Uninsured/Underinsured Motorist | Is this coverage available, required, optional, or automatically included in my state? | It may help when another driver has no insurance or not enough insurance. |

| Medical-Related Coverage | Does the quote include medical payments, PIP, or a similar coverage? | Rules and availability can vary by state and policy type. |

| Rental, Towing, or Roadside | Are these included, optional, or unavailable? | Small add-ons can affect both convenience and total premium. |

For a deeper coverage breakdown, review our guide to auto policy options.

Information to Prepare Before Requesting a Quote

A cleaner quote process usually starts with accurate information. If details are missing or estimated, the final premium can change after underwriting, verification, or document review.

- Driver informationNames, dates of birth, license status, and driving history for household drivers.

- Vehicle detailsVIN, year, make, model, mileage, ownership, and garaging address.

- Prior insuranceCurrent insurer, policy expiration date, and any lapse in coverage.

- Coverage preferencesDesired limits, deductibles, optional add-ons, and lender requirements.

- Payment preferenceDown payment, monthly installment needs, or paid-in-full preference.

- Use of vehicleCommuting, personal use, business use, delivery work, or rideshare use.

If you need a faster quote path, our instant car insurance quote guide explains what drivers usually need before comparing same-day options.

How to Compare Quotes From an Agency Fairly

Two quotes can look similar but provide very different protection. Before choosing one, compare the same limits, deductibles, drivers, vehicles, optional coverages, fees, and payment schedules.

| Comparison Point | What to Review | Common Mistake to Avoid |

|---|---|---|

| Coverage Limits | Compare bodily injury, property damage, and uninsured motorist limits. | Choosing the cheapest quote without noticing lower limits. |

| Deductibles | Check collision and comprehensive deductibles. | Assuming a cheaper premium is better when the deductible is much higher. |

| Fees and Installments | Review billing fees, installment fees, down payment, and total policy cost. | Focusing only on the first payment or monthly price. |

| Exclusions | Review excluded drivers, business use restrictions, delivery use, and special vehicle use. | Finding out after a claim that a use or driver was excluded. |

| Claims Process | Ask who handles claims and how to report an accident. | Assuming the agency and carrier have the same claim role. |

For broader shopping guidance, see our page on how to choose an insurance provider wisely.

Red Flags to Watch for Before Buying Coverage

A trustworthy quote process should be clear about who issues the policy, what the policy covers, what it excludes, how much it costs, and when coverage begins. Be cautious when important details are vague or when a quote relies on unrealistic promises.

Unverified Price Promises

Be careful with claims like guaranteed low rates, very low down payments, or savings amounts that are not supported by written quote documents.

No Carrier Name

Ask which insurance company will issue the policy. The agency or website may not be the actual insurance carrier.

Pressure to Pay Quickly

Do not rush payment before reviewing coverage, fees, cancellation terms, and proof that coverage will start.

No Written Documents

Save the quote, declarations page, policy documents, receipts, ID cards, and all confirmation emails.

Payment and Discount Questions to Ask

Discounts and payment plans vary by insurer, state, driver profile, and eligibility. Instead of relying on generic discount claims, ask which savings appear in your actual quote and whether the full-term policy cost changes under different payment structures.

- Down paymentHow much is due today to start coverage?

- Installment feesAre there fees for paying monthly?

- Paid-in-full optionIs there a lower total cost if I pay the policy in full?

- Automatic paymentsDoes autopay affect price or billing reliability?

- Discount verificationWhich discounts are actually included in this quote?

- Cancellation termsWhat happens if I miss a payment or cancel early?

Cost reminder: A lower first payment does not automatically mean cheaper insurance. Compare the total premium, fees, coverage limits, deductible, and cancellation rules before choosing a policy.

Claims Support Questions to Ask an Agency

Claims are usually handled by the insurance carrier, but an agency may help explain how to contact the carrier, what documents to gather, and how to understand next steps. Before buying, ask what kind of support is available after an accident.

| Claims Question | Why to Ask It |

|---|---|

| Who do I contact after an accident? | You should know whether to call the agency, the carrier, a claims hotline, or use an app or online portal. |

| What documents should I save? | Photos, police reports when applicable, repair estimates, witness details, and claim numbers can matter. |

| Can I choose my repair shop? | Repair-shop rules vary by insurer and state, so ask before a claim happens. |

| Does rental reimbursement apply? | Rental coverage is often optional and may not be included unless selected. |

| How are claim updates delivered? | Ask whether updates come by phone, email, text, app, online account, or mail. |

For more claim-preparation guidance, see our guide to the insurance claims process.

Independent information notice: RodneyDYoung.org is an independent information website and is not an insurance carrier. Policy availability, underwriting approval, rates, discounts, fees, payment plans, and claim handling depend on the insurer and the driver’s eligibility.

Frequently Asked Questions

What does an insurance agency do?

An insurance agency may help customers compare available options, understand coverage choices, apply for policies, make changes, and identify the insurance carrier that will issue the policy. The exact role depends on licensing, carrier appointments, and state rules.

Is an insurance agency the same as an insurance company?

No. An agency may help sell or service policies, while the insurance company or carrier usually underwrites the policy and handles covered claims according to the policy terms.

How can I check whether an agent or company is licensed?

NAIC recommends checking with your state insurance department to confirm that the company and agent are licensed before buying insurance.[2]

Should I choose the lowest quote from an agency?

Not automatically. Compare coverage limits, deductibles, fees, exclusions, payment terms, and total policy cost. A lower quote may provide less protection or a higher deductible.

What should I ask before paying for a policy?

Ask which carrier issues the policy, when coverage starts, what is included, what is excluded, what fees apply, how cancellations work, and how to get proof of insurance.

Conclusion

Rodney D. Young Insurance Agency searches should lead drivers to evaluate the insurance shopping process, not just the lowest advertised price. A helpful agency or quote path should make it easier to understand who issues the policy, what coverage is included, what the exclusions are, how much the policy costs over the full term, and how support works after purchase.

Before starting coverage, verify licensing where appropriate, compare quotes with the same limits and deductibles, ask about the insurance carrier behind the policy, review payment terms carefully, and save all written documents. The best insurance decision is usually the one that balances affordability, legal compliance, and meaningful protection.

Explore Auto Insurance Quote Options

Enter your ZIP code to compare available quote paths and review coverage options, payment structures, and policy choices with more clarity.

References

- National Association of Insurance Commissioners. “How to Choose an Insurance Agent.” Source ↩

- National Association of Insurance Commissioners. “Protect Yourself: Buying Insurance on the Internet.” Source ↩

- National Association of Insurance Commissioners. “Auto Insurance.” Source ↩

- Insurance Information Institute. “Auto Insurance Basics: Understanding Your Coverage.” Source ↩