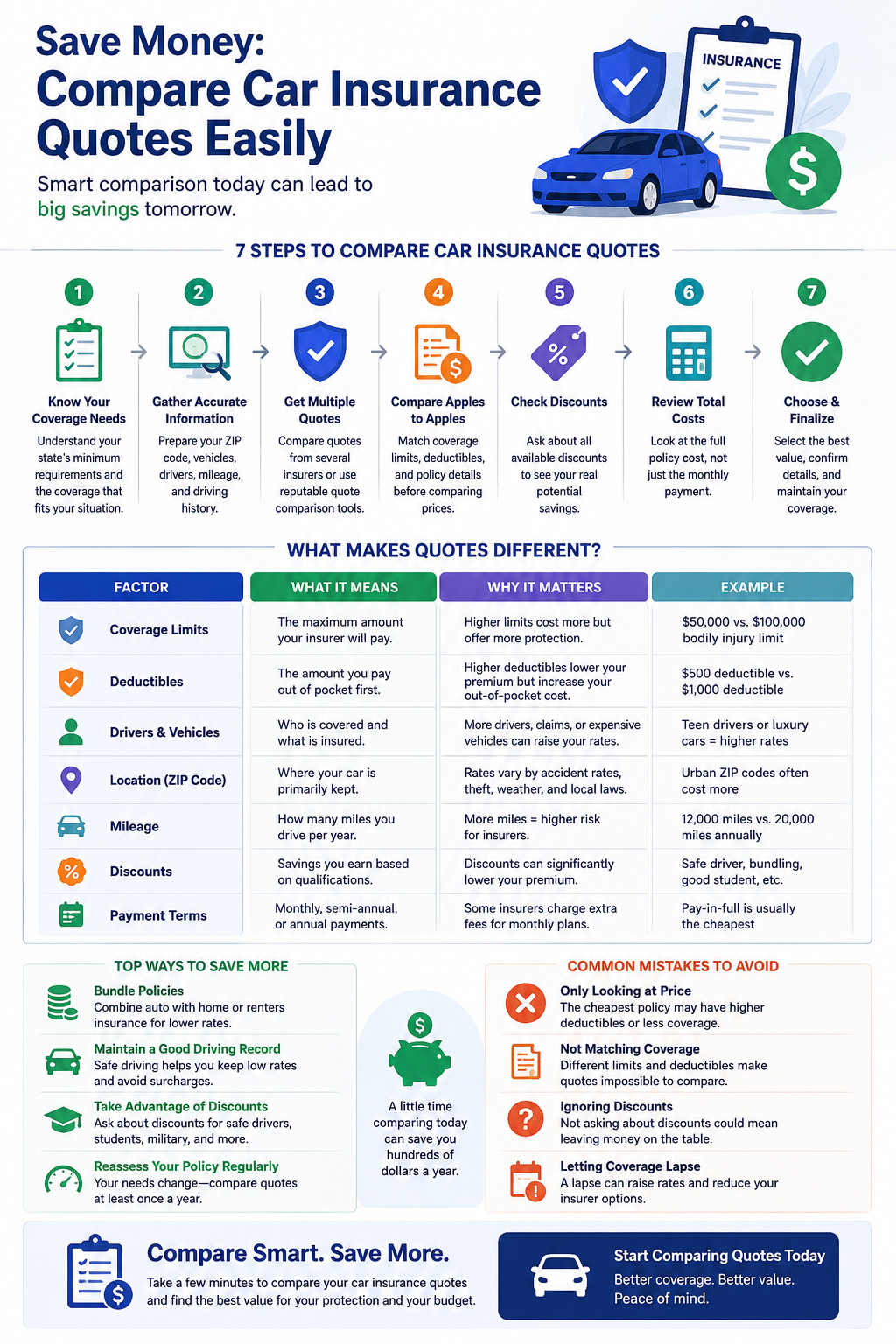

Comparing car insurance quotes can help drivers find a policy that fits their budget, but the cheapest number on the screen is not always the best choice. A quote can look lower because it has weaker liability limits, higher deductibles, fewer optional coverages, different drivers listed, or a payment schedule with extra fees.

The right way to compare car insurance quotes is to match the same driver information, vehicle details, ZIP code, coverage limits, deductibles, payment terms, and discounts across every quote. Then you can review the total cost and coverage quality instead of choosing based only on the monthly premium.

Quick Summary

- Compare at least three quotes using the same coverage limits, deductibles, drivers, vehicles, ZIP code, and mileage assumptions.

- Review the total six-month or twelve-month premium, not only the first payment or monthly payment.

- Ask which discounts are already included and which require proof, such as safe-driver, multi-policy, low-mileage, student, telematics, autopay, or paperless billing discounts.

- Do not lower liability limits or raise deductibles only to make a quote look cheaper.

- Check cancellation rules, billing fees, installment fees, claim reporting options, and insurer service quality before switching.

- Re-shop after major life changes, renewals, moves, vehicle changes, clean driving periods, or when new discounts may apply.

Auto insurance pricing can vary widely because insurers weigh driver, vehicle, location, coverage, and billing factors differently. The Insurance Information Institute explains that auto insurance prices may be affected by driving record, vehicle use, location, age, vehicle type, credit-based insurance information where allowed, coverage type, limits, and deductibles.[1]

Because every insurer uses its own rating approach, comparing only one company can leave savings opportunities hidden. At the same time, a lower quote is only useful if it still provides the coverage you need and a payment schedule you can maintain. For a deeper coverage checklist, review how to compare auto insurance policies by key features.

Why Comparing Car Insurance Quotes Matters

Shopping around matters because two companies can price the same driver differently. One insurer may offer a better rate for a clean driving record, while another may be more competitive for a household with multiple vehicles, a student driver, low annual mileage, or a specific vehicle type.

The National Association of Insurance Commissioners recommends comparing quotes from multiple insurance companies and making sure the quotes include the same coverage, limits, and deductibles.[2] That “same coverage” part is important. If one quote has state minimum liability and another includes higher liability limits plus collision and comprehensive coverage, the prices are not directly comparable.

Important coverage note

A cheap quote is not automatically a better quote. If the lower price comes from reduced liability limits, missing physical damage coverage, or a deductible you could not afford after a claim, the policy may create more financial risk than it removes.

What to Compare Across Car Insurance Quotes

A fair comparison starts with matching the details. Small quote differences can change the final price and make one offer look better than it really is.

| Quote detail | Why it matters | What to check |

|---|---|---|

| Liability limits | Lower limits may reduce price but increase your exposure after a serious accident. | Match bodily injury and property damage limits across every quote. |

| Deductibles | Higher deductibles may reduce premium but increase your out-of-pocket cost after a covered claim. | Compare collision and comprehensive deductibles side by side. |

| Collision and comprehensive | These coverages may matter for financed, leased, newer, or valuable vehicles. | Confirm whether they are included or excluded. |

| Uninsured or underinsured motorist coverage | This coverage may protect you if another driver has no insurance or not enough insurance, depending on state rules and policy terms. | Check whether it is included, rejected, optional, or required in your state. |

| Drivers and vehicles listed | Missing household drivers or vehicles can make a quote inaccurate. | Make sure every regular driver and vehicle is listed correctly. |

| ZIP code and garaging address | Location can affect theft risk, claim frequency, repair costs, and available carriers. | Use the address where the vehicle is primarily kept. |

| Total premium and payment plan | A low first payment may not mean the lowest total cost. | Compare the total policy term, first payment, installments, and fees. |

Rate, Quote, Premium, and Coverage: What These Terms Mean

Drivers often use “rate,” “quote,” and “premium” as if they mean the same thing, but they are not identical. Understanding the difference can make quote comparison easier.

An estimated policy price based on the information entered. The final premium can change after underwriting or verification.

The amount charged for the policy term or billing period, before or after fees depending on how the quote is displayed.

The protection purchased, including limits, deductibles, exclusions, optional coverages, and policy conditions.

Comparison rule

Compare price only after the coverage is aligned. A lower quote with weaker coverage is not the same offer as a higher quote with stronger protection.

How Car Insurance Premiums Are Usually Calculated

Every company uses its own pricing model, but common factors can include driving record, claim history, prior insurance, ZIP code, vehicle type, vehicle use, annual mileage, selected coverage, deductible amounts, and credit-based insurance information where allowed by state law.

NAIC explains that the amount paid for auto insurance depends on the coverage selected and how risky the company believes the driver is to insure.[3] That is why the same driver may see different quotes from different insurers, even when the same coverage is requested.

| Pricing factor | How it may affect quotes | Shopping tip |

|---|---|---|

| Driving record | Tickets, accidents, and claims may increase price. | Re-shop after violations or claims age out of the rating period. |

| Vehicle | Repair cost, theft risk, safety features, and vehicle value can affect premium. | Compare insurance costs before buying a different car. |

| Annual mileage | Lower mileage may qualify for savings with some insurers. | Ask whether mileage must be verified. |

| Coverage limits | Higher limits usually cost more, but may provide stronger protection. | Choose limits based on risk, not only monthly price. |

| Deductibles | Higher deductibles may lower premium but increase claim costs. | Choose a deductible you could realistically pay. |

| Payment method | Autopay, paperless billing, installment billing, or paid-in-full options can affect cost. | Ask whether payment method changes fees, discounts, or total price. |

How to Compare Quotes Without Getting Misled

The easiest mistake is comparing monthly payments instead of the full policy. One quote may show a smaller first payment but higher installments later. Another may have a higher first payment but lower total cost over six or twelve months.

- Choose a coverage baseline. Decide which liability limits, deductibles, and optional coverages you want before requesting quotes.

- Use the same driver and vehicle details. Keep vehicle use, garaging address, mileage, and listed drivers consistent.

- Compare the total policy cost. Review the full premium, first payment, monthly installments, policy fees, billing fees, and cancellation terms.

- Ask which discounts are included. Do not assume discounts were automatically applied.

- Review coverage exclusions and optional benefits. Roadside assistance, rental reimbursement, gap-related coverage, and towing may differ by quote.

- Confirm the effective date. If switching, make sure the new policy starts before canceling the old policy.

If you need a quote quickly because you are buying a car, replacing a policy, or avoiding a coverage gap, review this guide to getting an instant car insurance quote so you understand the difference between a quote, payment, effective date, and active proof of insurance.

Discounts That May Lower Your Car Insurance Quote

Discounts can reduce the premium for eligible drivers, but availability varies by company and state. The Insurance Information Institute lists several ways drivers may lower auto insurance costs, including shopping around, comparing insurance costs before buying a car, using higher deductibles carefully, bundling policies, maintaining a good credit record where allowed, and asking about low-mileage or group discounts.[4]

| Discount category | Who may benefit | Question to ask |

|---|---|---|

| Safe-driver discount | Drivers with clean records or fewer recent violations. | How far back does the company review tickets, crashes, or claims? |

| Multi-policy discount | Drivers who bundle auto with homeowners, renters, condo, or other coverage. | Does bundling reduce the total cost across both policies? |

| Multi-car discount | Households insuring more than one vehicle. | Do all vehicles need to be on the same policy? |

| Good student discount | Eligible student drivers who meet the insurer’s academic rules. | What GPA, age, school status, or proof is required? |

| Low-mileage discount | Drivers who drive less than average or keep a vehicle mostly parked. | How is mileage verified? |

| Telematics discount | Drivers willing to use a driving app or device. | Can driving data increase the rate, or only reduce it? |

| Autopay or paperless billing | Drivers who use automatic payments or electronic documents. | Does this lower the premium, reduce a fee, or simply change billing? |

For a brand-focused option to compare during your quote search, review Rodney D. Young auto insurance while keeping the same limits, deductibles, drivers, vehicles, ZIP code, and payment assumptions across each quote.

Deductibles and Limits Can Change the Price Quickly

Deductibles and liability limits are two of the biggest reasons quotes may look different. A higher deductible may lower the premium, but it also increases what you may owe after a covered collision or comprehensive claim. Lower liability limits may reduce the price, but they can leave you exposed after a serious accident.

The Insurance Information Institute notes that choosing a higher deductible can reduce costs, but drivers should have enough money set aside to pay the deductible if they have a claim.[4] Before raising a deductible, decide whether that out-of-pocket amount is realistic.

Do not cut protection blindly

Lowering coverage only to reduce the quote can make the policy look cheaper while increasing your financial risk. Match coverage first, then compare the premium.

Before choosing a higher out-of-pocket amount, compare the deductible against the premium savings, vehicle value, claim risk, and whether you could realistically pay that amount after a covered loss.

Payment Plans, First Payments, and Total Cost

Drivers often compare the monthly payment because it is the easiest number to understand. However, the monthly payment may not show the full policy cost. A quote can include a first payment, installment charges, billing fees, late fees, or different payment schedules.

Compare the payment schedule

- Amount due today.

- Total six-month or twelve-month premium.

- Each monthly installment after the first payment.

- Installment, billing, processing, or late fees.

- Whether autopay or paperless billing changes the cost.

- Whether paying in full avoids fees or qualifies for a discount.

If you are comparing quotes for a teen, student, or newer driver, review cheap car insurance for young drivers because age, driving experience, school status, household policy setup, and vehicle choice can affect the final quote.

Information to Have Ready Before Comparing Quotes

Accurate information helps prevent quote changes later. Before using a quote form or speaking with an agent, gather the details insurers commonly request.

Quote preparation checklist

- Driver names, dates of birth, and license information.

- Vehicle year, make, model, and vehicle identification number.

- ZIP code and garaging address.

- Estimated annual mileage and vehicle use.

- Current or prior insurance information, if available.

- Recent tickets, accidents, or claims.

- Desired liability limits, deductibles, and optional coverages.

- Lender or leaseholder information if the vehicle is financed or leased.

When to Compare Car Insurance Quotes Again

Comparing once is useful, but insurance pricing changes. You may find a better fit after a renewal, a move, a vehicle change, a clean driving period, or a household change.

Review the renewal premium before accepting it automatically.

A new ZIP code or garaging address can change available carriers and prices.

Insurance costs can vary significantly by vehicle.

Adding or removing drivers, changing mileage, or buying a home can affect discounts and rates.

Common Mistakes to Avoid When Comparing Quotes

Quote comparison mistakes

- Comparing quotes with different liability limits or deductibles.

- Choosing the lowest price without checking missing coverages.

- Ignoring the total policy cost and focusing only on monthly payments.

- Forgetting to ask whether discounts are already included.

- Entering different mileage, vehicle use, or driver details across quote forms.

- Canceling an old policy before the new policy is active.

- Choosing a deductible that would be hard to pay after a claim.

- Ignoring claim service, billing terms, cancellation rules, and insurer reliability.

Special Rate Factors for Young Drivers

Young drivers may need a more specific comparison strategy because age, driving experience, student status, household policy setup, vehicle choice, and telematics can affect quotes. When a teen, student, or driver under 25 is included, compare the same coverage assumptions carefully before choosing based only on monthly price.

This page focuses on general quote comparison for all drivers. The young-driver guide covers student discounts, parent-policy decisions, telematics, vehicle choice, and other rate factors that are more specific to younger drivers.

FAQ About Comparing Car Insurance Quotes

How many car insurance quotes should I compare?

It is usually smart to compare several quotes from different insurers. Make sure each quote uses the same drivers, vehicles, ZIP code, liability limits, deductibles, mileage, and optional coverages before comparing price.

Should I choose the cheapest car insurance quote?

Not automatically. The cheapest quote may have lower limits, higher deductibles, fewer coverages, or different fees. Compare coverage quality and total cost before choosing.

Does comparing car insurance quotes affect my credit?

Requesting auto insurance quotes is generally different from applying for credit. However, some insurers may use credit-based insurance information where allowed by state law. Ask the insurer how quote and rating information is used in your state.

Why are two car insurance quotes so different?

Quotes can differ because insurers weigh driving record, location, vehicle, mileage, prior insurance, coverage limits, deductibles, discounts, payment method, and underwriting rules differently.

What details should match when I compare quotes?

Match the same liability limits, deductibles, drivers, vehicles, garaging address, mileage, vehicle use, optional coverages, and payment assumptions.

How often should I compare car insurance quotes?

Compare at renewal and after major changes such as moving, buying a different vehicle, adding or removing a driver, improving your driving record, changing mileage, or qualifying for new discounts.

Can discounts change after I buy the policy?

Yes. Some discounts can change at renewal or after the insurer reviews proof, driving data, mileage, household information, billing status, or policy changes.

What should I do before switching companies?

Confirm the new policy’s effective date, amount due, coverage limits, deductibles, cancellation rules, and payment schedule before canceling the old policy. Avoid creating a lapse in coverage.

Conclusion

Comparing car insurance quotes can help drivers save money, but the comparison only works when the quotes are built on the same assumptions. Match coverage limits, deductibles, drivers, vehicles, ZIP code, mileage, discounts, and payment terms before deciding which policy is truly cheaper.

The best quote is not always the smallest monthly payment. It is the policy that balances price, coverage, deductibles, payment schedule, insurer reliability, and your real financial risk. Review your options regularly, ask about discounts, and avoid reducing important protection only to make a quote look lower.

Compare Auto Insurance Quote Options

Enter your ZIP code to begin comparing available auto insurance quote paths. Review coverage limits, deductibles, payment terms, discounts, and total policy cost before choosing a policy.

References

- Insurance Information Institute, “What Determines the Price of My Auto Insurance Policy?” ↩

- National Association of Insurance Commissioners, “A Shopping Tool for Auto Insurance.” ↩

- National Association of Insurance Commissioners, “Auto Insurance.” ↩

- Insurance Information Institute, “Nine Ways to Lower Your Auto Insurance Costs.” ↩ ↩